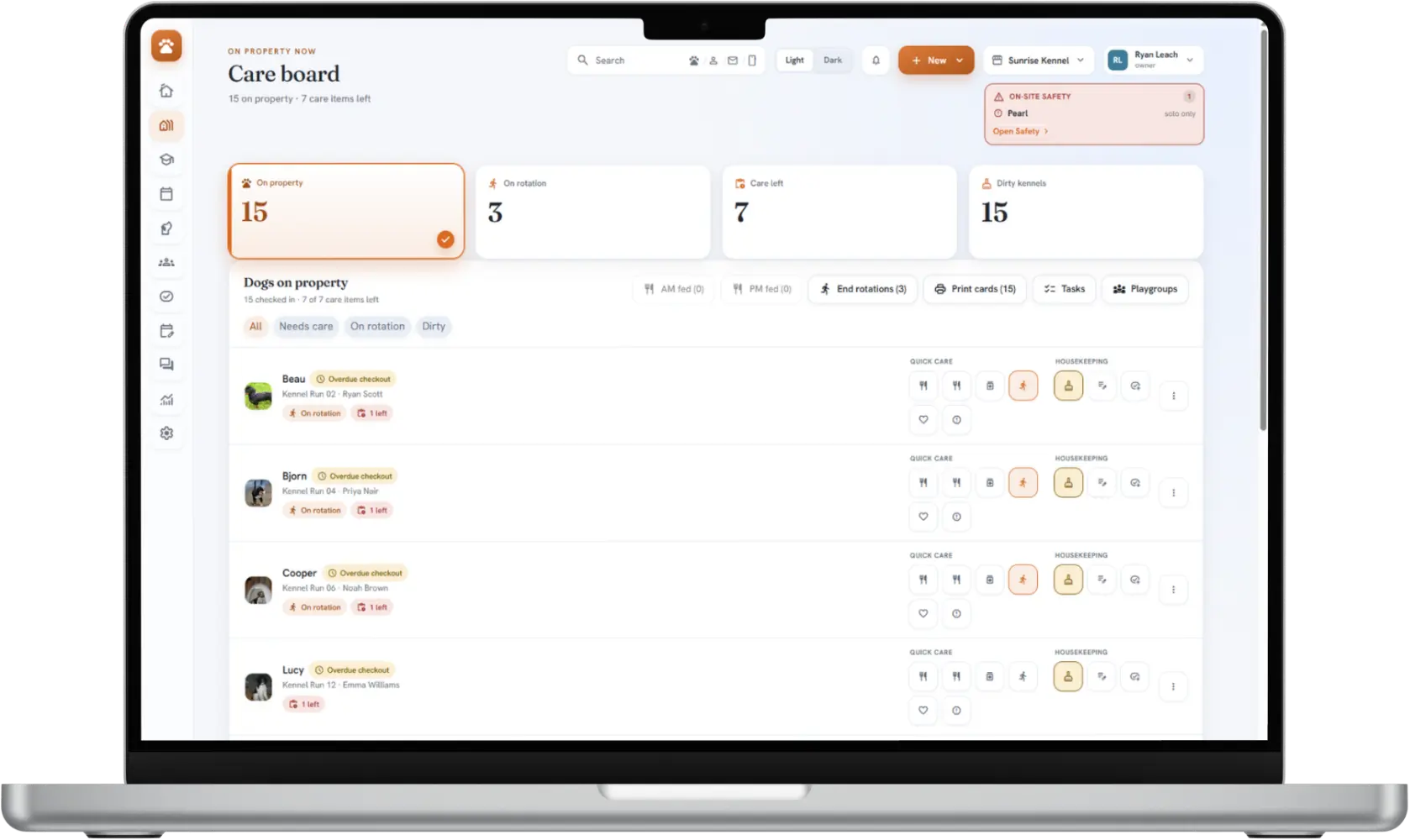

Renewal creep

The price you signed up at isn't the price three years in. Increases tend to arrive at renewal — the exact moment switching is most painful and you're least likely to walk.

For most of the tools you know in pet care, the answer is a private-equity fund or a venture board — and that quietly shapes your prices, your payments, your support, and what gets built next. BarkWhiz is the exception: bootstrapped and founder-owned, with no outside investors. Here's the difference — and why you feel it.

Most operators never stop to ask it, but it shapes everything downstream: who owns the company behind the software running your business? In pet care, the answer is increasingly an investor — and it's all publicly reported.

Start with the biggest name. Togetherwork, a platform backed by the private-equity firm Aquiline Capital Partners, has quietly assembled a stable of kennel-software brands. It bought Gingr in 2017, added PetExec in late 2024, and also owns Revelation Pets — three of the names operators shop between, now under one PE-backed roof serving a reported 7,000+ pet-care businesses.

Look at how that platform describes itself: the leader in “software and payments” for pet care. That second word is the tell. The private-equity playbook for vertical software isn't just to sell you a subscription — it's to sit in the middle of every payment your customers make and take a cut of it. Once the company behind your software answers to a fund's return target, the levers are predictable, and none of them are pointed at you.

None of this is unique to one brand — it's the pattern operators across acquired vertical software tend to feel on the ground:

The price you signed up at isn't the price three years in. Increases tend to arrive at renewal — the exact moment switching is most painful and you're least likely to walk.

Pressure to route your customers' payments through the platform's own processing, at the platform's rates — because that transaction cut, not your subscription, is where the real margin lives.

The person who used to answer becomes a ticket queue. As a brand folds into a bigger portfolio, help tends to feel slower, more scripted, and a step removed from anyone who actually runs a facility.

Your feature requests now compete with whatever grows platform revenue. What ships is what monetizes the portfolio — not necessarily the thing you asked for.

To be fair: consolidation can bring real resources, and Togetherwork says it keeps each brand's support separate and that the deals let it deliver better products and innovation. The owners aren't villains — that's why our even-handed Gingr comparison is upfront about what Gingr does well. The point isn't who they are — it's who the software answers to. A fund's job is the return, and that's the incentive every decision gets weighed against.

And it isn't only the roll-ups. The newer challengers are venture-funded — Goose raised a reported $13.4M seed round in early 2025, and MoeGo a $24M Series A led by Base10 (both publicly reported). That's not a knock; outside capital can fund real progress. But it puts the same kind of people in the room: investors who own a piece, and a board that expects a return on it. If you don't want to sell to a roll-up, it's worth asking whether you want to depend on anyone's cap table for the software that runs your floor.

Acquired or venture-funded, the other names in pet care juggle shareholders, board members, and customers. We focus on the ones who matter most — you.

No private-equity owners. No outside investors. No board pushing for the next price increase or the forced payment switch. BarkWhiz is funded by the founder — a working pet-care operator — and built for the people who want to stay independent and run a tight ship, not get absorbed into someone else's portfolio.

Founding facilities receive Ops + CRM for $249/month, locked for 24 months. After that, they retain a permanent 15% discount from the then-current list price.

An honest note, because we hold this line everywhere: we're early, we're small, and we'd never pretend otherwise — QuickBooks is the one operator-facing integration live today (under the hood, Stripe, Twilio, and Resend power payments, texting, and email), and we'll always tell you exactly what's ready. Being independent isn't a feature list; it's who we answer to.

The software is one front. The other is the buildings themselves — the same private-equity money is rolling up boarding, daycare and grooming facilities into national chains. It's the backdrop every independent is now operating against.

U.S. grooming & boarding establishments — none above 5% market share (Ankura)

2024 pet boarding — the largest services slice, with PE-backed platforms the active buyers (Capstone)

one platform's locations after 42 acquisitions in 18 months (Best Friends, M&A)

Pet Resort Hospitality Group (PE-backed) has built a 40-resort portfolio in about two years; the 200-plus-location Camp Bow Wow franchise is now PE-owned. Advisors call it “early innings” — there's a lot more buying to come. If you're ready to sell, that's genuinely good news. If you'd rather stay independent, read on.

The platforms' edge is operational tightness — consistent systems, less leakage, professional follow-up. The good news for independents: that's software, not size. You can run that tight without giving up ownership.

Reservations, the care floor, and customer records in one connected place — the kind of operational consistency the platforms standardize, without a head office telling you how to run your facility.

The AI drafts the next pet-parent update or rebooking nudge; you review and send. The repeat-business engine the chains invest in — in the hands of the owner who actually knows the dog.

Independence is the thing a roll-up can't sell back to a community. Keep the relationship and the local character — and let the software carry the operational load.

More on the independent, operator-owned story → · How switching works →

Founding facilities receive Ops + CRM for $249/month, locked for 24 months. After that, they retain a permanent 15% discount from the then-current list price.

We reply within two business days—or your first month is free. No credit card required.

Not ready for a founding spot? Just keep me posted

For the folks who want to read the primary material themselves. These are the M&A advisors, analysts and trade outlets tracking the consolidation wave — not us paraphrasing it.

A fair caveat: mainstream national coverage of this trend is still thin — most of the documentation lives in M&A trade press, advisory-firm research and company deal releases. Figures are as reported by the sources above and reflect the dates of those reports.